simonkr/E+ via Getty Images

Summary of investments

After a strong 2nd quarter, RadNet, Inc. (NASDAQ:RDNT) continued its longer-term operating trends and injected significant amounts of cash into and below the bottom line. RDNT presents with the desirable equity premiums that investors pay a premium for FY22. We believe it is well positioned to benefit from industry tailwinds in the Covid-19 rebound, and given its offering in medical imaging, it is well differentiated in the healthcare space. health.

Imaging is linked to a multitude of medical and paramedical fields which extract innumerable sources of income. It is also a need for specialized medical treatment in almost all cases, and remains about as defensive as possible. Valuations suggest it is currently fair and reasonably priced, which is conducive to opening or re-allocating RDNT to equity risk. On this point, we rate RDNT as a buy.

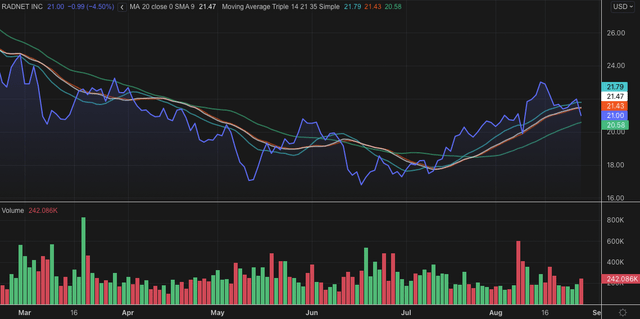

Exhibit 1. RDNT 6 month price action

Stocks have caught a bid since July and climbed back above key moving averages, indicating market psychology around the stock

Data: Refinitiv Eikon

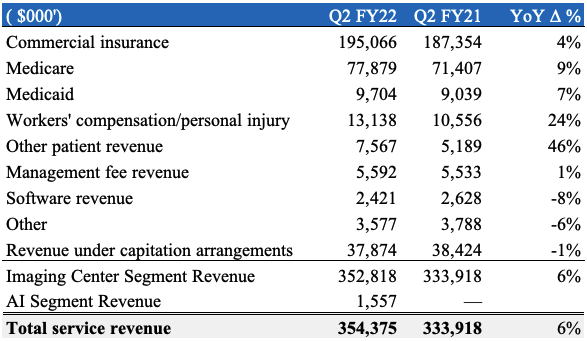

The strength of Q2 earnings in full view

Second-quarter earnings were strong, with gains above consensus at the high and low levels. Revenue was $354 million, up about 610 basis points, including recorded revenue from its AI segment. Imaging center revenue printed $352 million, up about 570 basis points year-on-year. As shown in Table 2, growth was seen in most operating segments, with a particular increase in workers’ compensation and commercial insurance. Meanwhile, software revenue fell about 600 basis points year-over-year, while management fee revenue was flat year-over-year.

Chart 2. Growth shown across a broad spectrum of the portfolio, with single-digit declines in small segments.

Data: RDNT Q2 FY22. Image: HB Insights US Equity Strategy

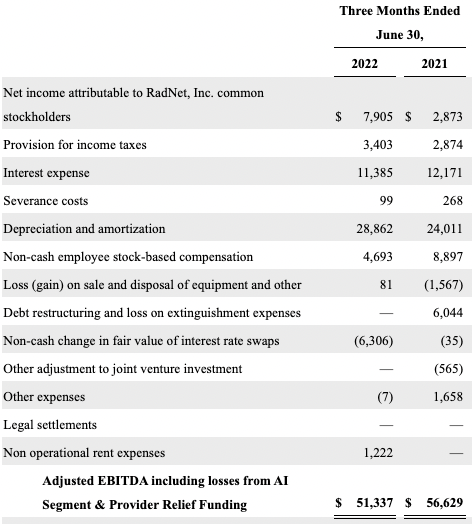

RDNT speaks in terms of Adjusted EBITDA (non-GAAP) as a measure of business performance, and it printed $51.3 million at that level including losses from its AI segment, compared to $56.6 million. dollars for FY21. On closer inspection, we believe this is a fair measure, with a few exceptions. The company reduced its stock-based compensation expense by approximately 47% year-over-year to $4.7 million, although it recognized approximately $4.85 million in additional non-cash amortization charges . It also elected to expense a $6.3 million gain on the fair value of its interest rate swaps.

As shown in Table 3, this figure is significantly higher than in the second quarter of FY21, due to the swap pricing mechanics tilting in favor of RDNT over its counterparty. To explain, from ~FY19 to Q1 FY21, the company had a large outflow related to being swap downside. However, as one-month LIBOR and SOFR have tipped higher, this now favors RDNT in each of its swap deals. It has $100 million of floating rate exposure at 1.96% and an additional $400 million at 2.05%, maturing in October 2022 and October 2025 respectively. Each of them is now in the money. RDNT is now receiving payment from each of its counterparty swaps, as per the second quarter earnings call. Treating SBC as an expense in both periods and removing the loss on debt restructuring from FY21 results, we see non-GAAP EBITDA of $47 million in the second quarter of FY22, compared to $41.6 million in the second quarter of FY21.

Piece 3.

Data: RDNT 10-Q Q2 FY2022

Drilling down into specific operational data, the results show that growth trends have been positive over the 12 months. Routine imaging fueled the bolus of procedure volumes, nearly 2.3 million in total. MRI and CT volumes increased by 770 bps and 700 bps, respectively, while PET volume increased by 10.4% year-on-year. Considering all imaging segments, volumes gained approximately 450 bps year-over-year. The increase in numbers caused accounts receivable to be mismatched against revenue reported for FY21, with accrued liabilities on trade accounts increasing by $31 million to $166 million.

Despite the increase, the number of days pending sales (“DSO”) declined to near-record levels for the company at approximately 39 days at the end of the second quarter of FY22. The improved result adds to an already impressive negative cash conversion cycle of 39 days. Translated, this means that RDNT is paid on average about 40 days before performing the revenue-related service. With a large portion of its income coming from insurance, workers’ compensation and health insurance, this ensures that the company will continue to enjoy favorable payment terms, being paid before the end of service in mean.

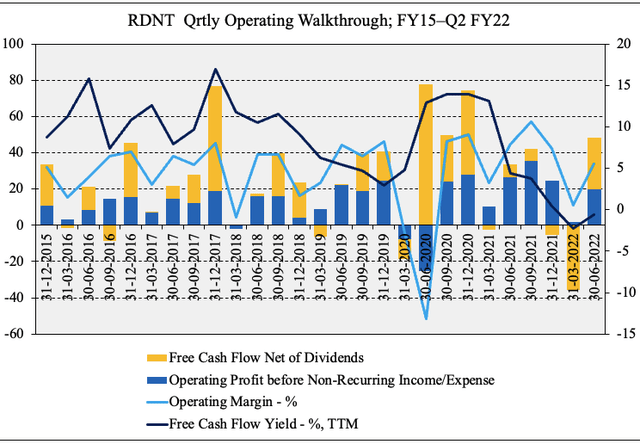

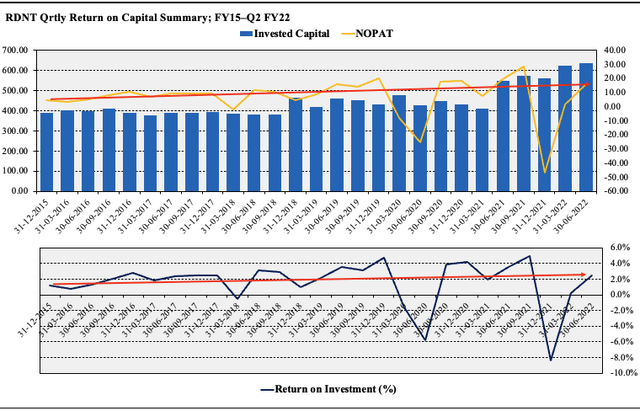

Therefore, operating metrics remain an attractive feature for RDNT. As shown in Exhibit 4, the company continues to hold the Maginot Line with its operating margin and pushed $28.7 million [$0.50/share] in FCF below net income in Q2 FY22. Despite the FCF yield shrinking in recent periods, this has happened while RDNT’s return on investment has remained buoyant, as shown in Figure 5. This has allowed the firm to invest capital at an annualized return of around 8.25%, a step above its WACC of 8.1%. RDNT therefore brings a fundamental dynamic to the forward-looking regime, which interests us in the context of our US equity strategy.

Piece 4.

Data: RDNT SEC filings; HB Insights

Figure 5. Return on investment trends remain dynamic, even seasonal.

The results show that RDNT’s efforts to develop NOPAT sequentially since FY15. Its acquisition and growth strategy allows it to invest capital at ~2% per quarter [~8.25% annualized] on average – in line with its WACC of 8.1%.

Image and Data: HB US Equity Strategy

Evaluation

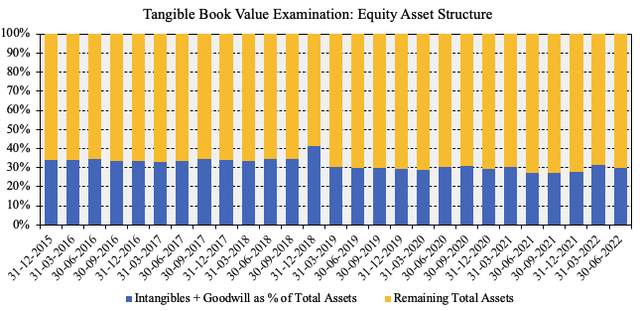

We got a respective upside in H2 FY22, tilting exposure to names that offer tangible sources of value in valuation. This includes [aside from DCF valuation, but this is sensitive to rates at present] cash flow and book value/tangible book value. RDNT has a negative tangible book value of equity, however, the percentage of assets, goodwill and intangible assets remains below 40%, as shown below.

This is attractive to us, compared to companies with similar business models in acquisitions and opening sites de novo, goodwill often skews the balance sheet. We believe that the company continues to pay reasonable prices for its acquisitions, given the percentage of goodwill it records on the balance sheet.

Exhibit 6. RDNT EX15–T2 EX22 Asset Structure

Data: HB Insights, RDNT SEC Filings

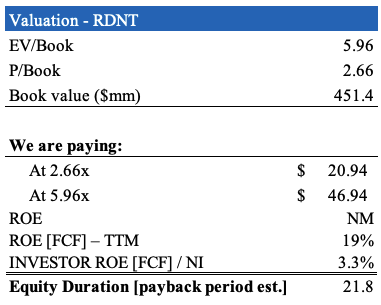

On that front, stocks look fairly priced at ~2.7x book value, although RDNT is also priced at ~6x EV/equity book value. If we were to pay this enterprise value, we would theoretically pay $47 per share, a substantial premium.

It should also be noted that the return on FCF equity for investors is only 3.3% on this valuation, ruling out the duration of equity. At 25x forward FCF estimates of $47 million, that puts RDNT at $21, and at 38x forward P/E, our FY23 EPS estimates put it at $22. Each of these suggests that we could pay a fair and reasonable price for the entry and/or reallocation of RDNT to our equity risk.

Piece 7.

Data: HB Insights

In short

We are bullish on RDNT stocks and believe the stock will catch a bid as part of a sector rotation into healthcare going forward. Investors are positioning themselves towards defensive sectors like healthcare and rewarding fundamentals within the space.

RDNT has several interesting features. Imaging is a multivariate service linked to a multitude of medical and paramedical fields. It has countless referral sources and is a necessity for specialized medical treatment in almost all cases. RDNT has additional features, in that, overall, it receives payment before the service is delivered. The shares also seem fair and reasonably priced. We RDNT rate a purchase.

Comments are closed.