David Gyung/iStock via Getty Images

A quick overview of Clearwater Analytics

Clearwater Analytics (NYSE: CWAN) went public in September 2021, raising approximately $540 million in gross proceeds from an IPO at a price of $18.00 per share.

The company offers automated services investment data aggregation, accounting, compliance, risk and reporting capabilities to financial institutions.

Although CWAN is essentially at operating breakeven and EPS, its stock isn’t cheap relative to a broader SaaS index, and the company’s growth rate will likely face pressure over the period. coming.

So I’m waiting for CWAN in the short term.

Introducing Clearwater Analytics

Clearwater, based in Boise, Idaho, was founded to develop a SaaS platform to simplify investment accounting and analysis for asset managers, insurance companies and large enterprises.

Management is led by CEO, Sandeep Sahai, who has been with the company since September 2016 and was previously CEO of Solmark, an investment partnership.

The company’s main offerings include:

-

Data aggregation

-

Investment accounting and reporting

-

Performance measurement

-

Compliance Monitoring

-

Risk analysis

The company maintains client relationships with asset managers, insurance companies and large corporations through a direct sales and marketing force that is focused on the United States.

Clearwater Analytics Market and Competition

According to a 2021 market research report by Market Primes, the global investment management software market was estimated at $3 billion in 2019 and is expected to reach nearly $4.5 billion by 2025.

This represents a projected CAGR of 10.2% from 2019 to 2025.

The main drivers of this expected growth are users’ desire to automate repetitive tasks so they can focus on optimizing portfolio performance and creating more sophisticated approaches.

Additionally, risk and exposure assessment and the ability to effectively report and share information with stakeholders will drive demand for better performing solutions.

Major competitors or other industry participants include:

-

SS&C

-

State Street

-

SAP

-

BNY Mellon (Eagle)

-

Simcorp

-

black rock

-

FIS

-

Northern Trust

-

Others

Clearwater Analytics Recent Financial Performance

-

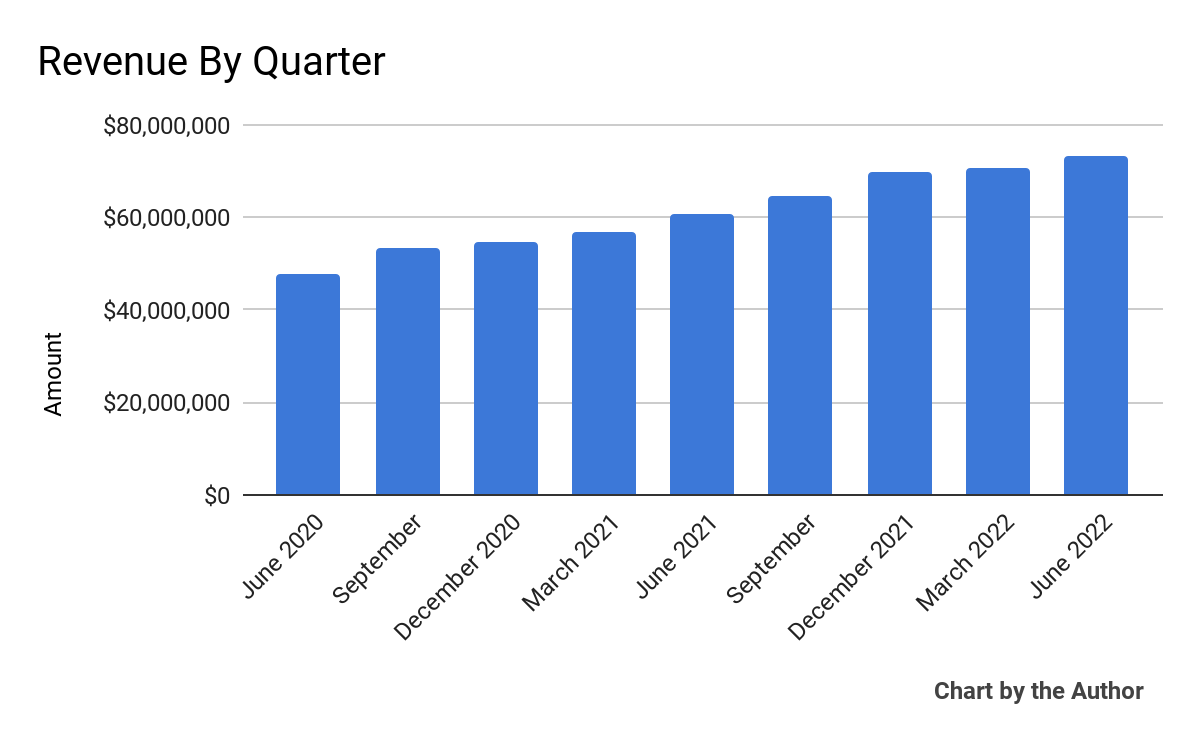

The total turnover per quarter increased according to the following graph:

Total revenue for the 9 quarters (looking for Alpha)

-

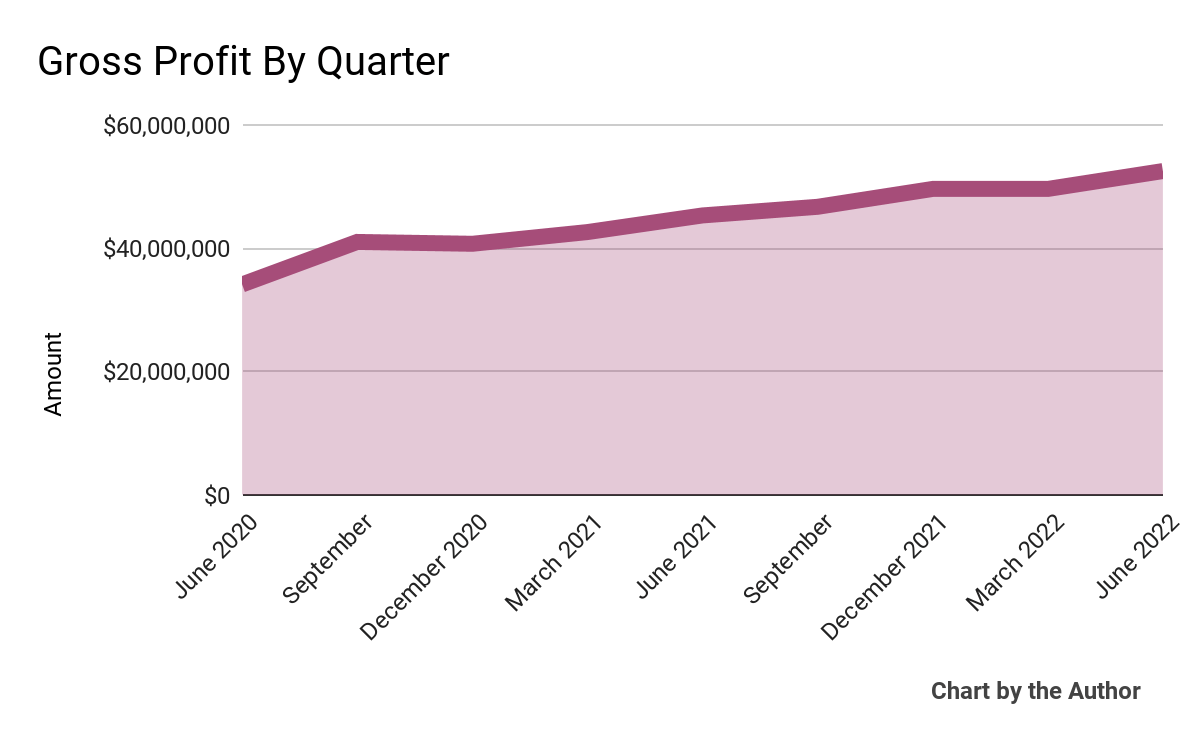

Gross profit per quarter increased on a similar trajectory:

Q9 gross profit (looking for Alpha)

-

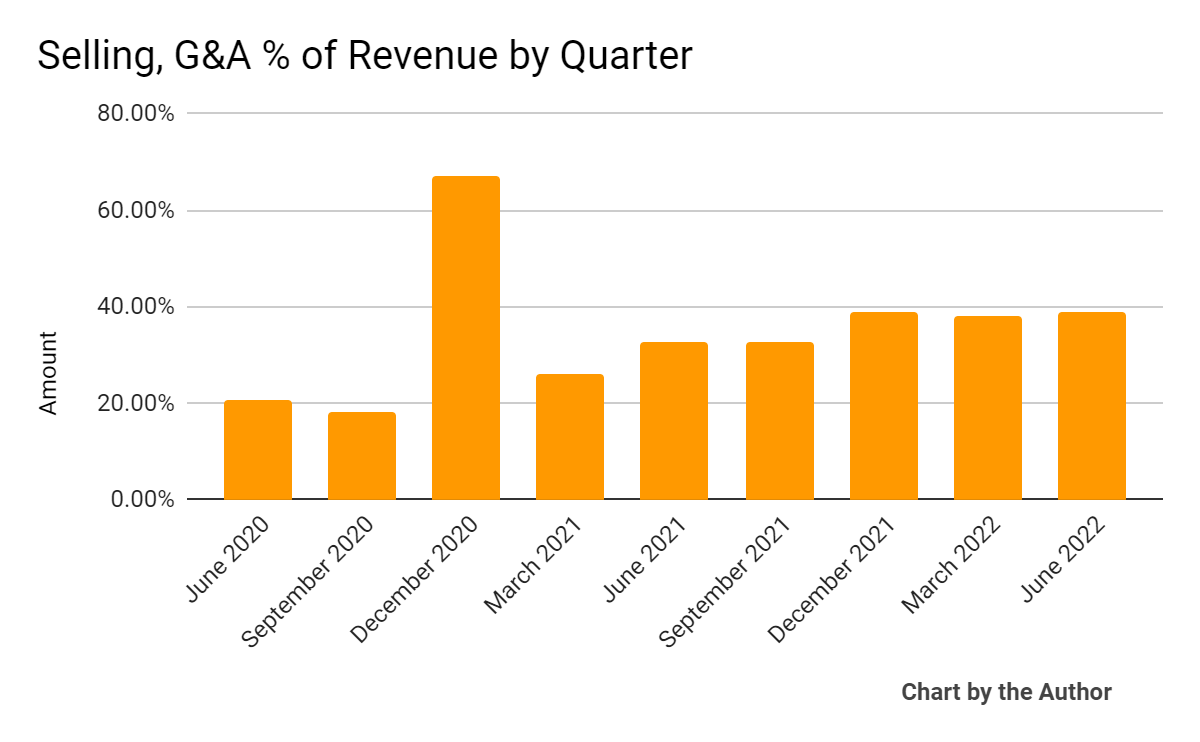

Selling, G&A expenses as a percentage of total revenue per quarter have increased in recent quarters:

9th Quarter Sales, G&A % of Revenue (Alpha Research)

-

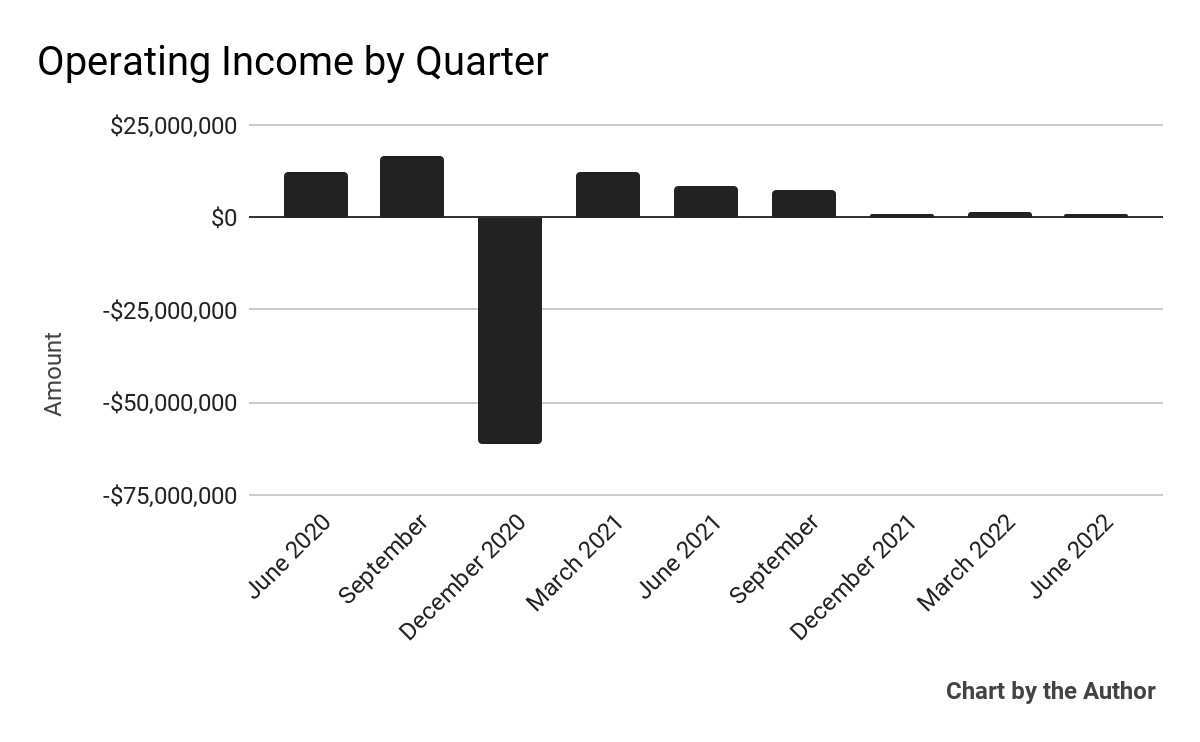

The operating result per quarter has remained negligible recently:

9th quarter operating profit (looking for Alpha)

(All data in the graphs above are in accordance with GAAP)

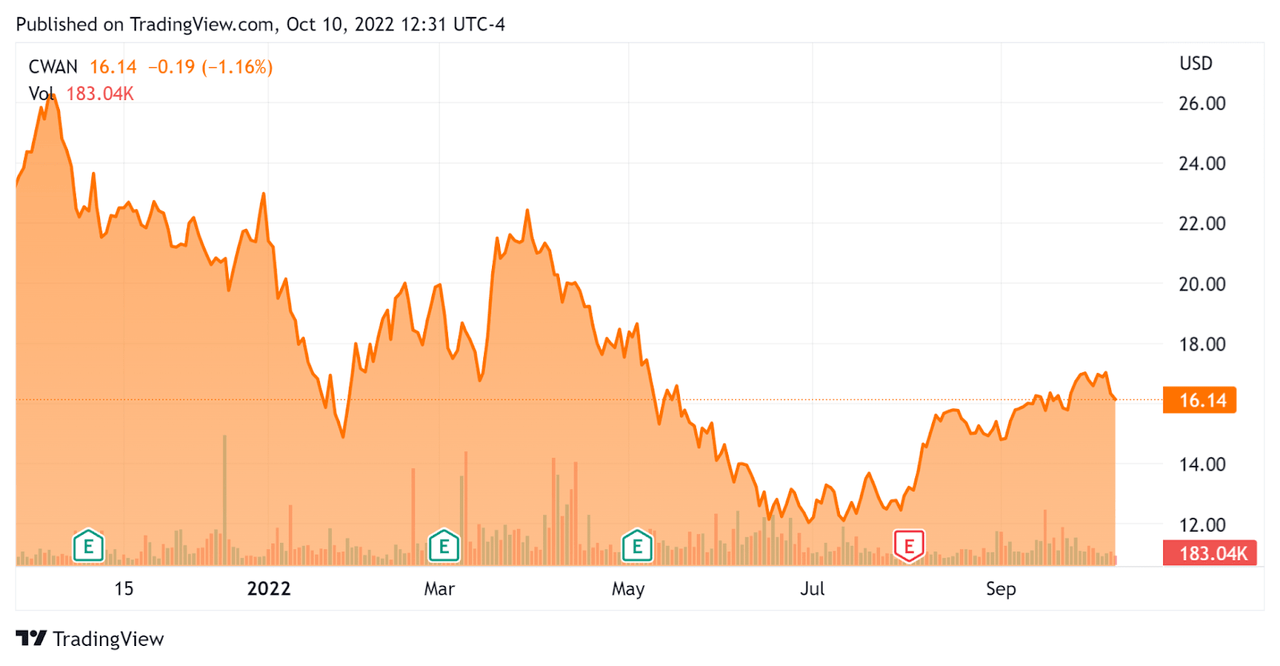

Over the past 12 months, CWAN’s stock price has fallen 30.3% compared to the US S&P 500 index decline of around 17.4%, as shown in the chart below :

52 week stock price (seeking alpha)

Valuation and Other Metrics for Clearwater Analytics

Below is a table of relevant capitalization and valuation figures for the company:

|

Measurement (TTM) |

Rising |

|

Enterprise Value/Sales |

10.50 |

|

Revenue growth rate |

23.3% |

|

Net profit margin |

-4.8% |

|

% EBITDA GAAP |

5.2% |

|

Market capitalization |

$3,880,000,000 |

|

Enterprise value |

$2,920,000,000 |

|

Operating cash flow |

$44,880,000 |

|

Earnings per share (fully diluted) |

-$0.05 |

(Source – Alpha Research)

The Rule of 40 is a software industry rule of thumb that states that as long as the combined revenue growth rate and EBITDA percentage rate are equal to or greater than 40%, the company is on a trajectory acceptable growth/EBITDA.

CWAN’s most recent GAAP Rule of 40 calculation was 28.5% in Q2 2022, so the company needs improvement in this regard, according to the table below:

|

Rule of 40 – GAAP |

Calculation |

|

Recent Rev. Growth % |

23.3% |

|

% EBITDA GAAP |

5.2% |

|

Total |

28.5% |

(Source – Alpha Research)

Clearwater Analytics Commentary

In its latest earnings call (Source – Seeking Alpha), covering Q2 2022 results, management noted that its AUM-based revenue model has come under pressure during recent periods of declining value. assets in the markets in which its clients operate.

In response, the company instituted a “fixed annual fee” for its core platform that is based on “the size and complexity of the customer portfolio.”

Management believes this change in revenue model will reduce volatility in its revenue growth trajectory and provide “a more predictable Net Revenue Retention (NRR) metric.”

As for its financial results, total revenue was up 21% year-over-year, with bookings being the highest in the company’s history.

The company’s net dollar retention rate decreased from 107% to 104%, due to a decrease in AUM values due to its aforementioned pricing structure which is currently undergoing a change.

The company’s Rule of 40 results need improvement. The gross margin was 75.7% while the adjusted EBITDA margin was 26%.

SG&A spending as a percentage of total revenue rose year-over-year, partly due to additional spending by public companies, and earnings per share fell into negative territory.

For the balance sheet, the company ended the quarter with $281.6 million in cash equivalents and short-term investments and $49.8 million in long-term debt.

In the past twelve months, free cash was $38.1 million, of which $6.8 was used for CapEx.

Looking ahead, management lowered its full-year revenue guidance to around 19% year-over-year growth in the mid-range, while Adjusted EBITDA is expected to be down. ‘about 80 million in the middle.

Stock-based compensation over the past 12 months was $57.2 million.

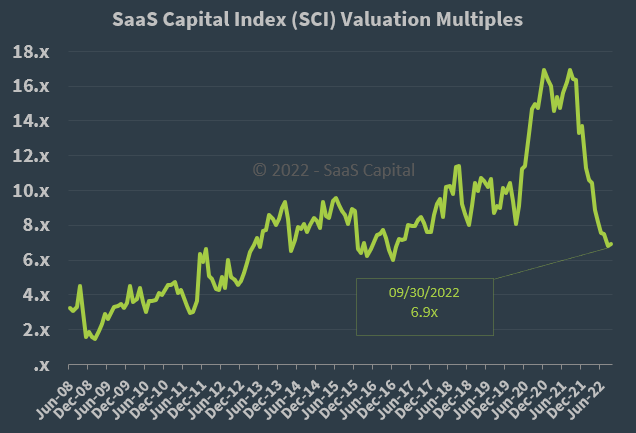

As for valuation, the market values CWAN at an EV/Sales multiple of around 10.5x.

The SaaS Capital Index of publicly held SaaS software companies had an EV/Average Revenue multiple of approximately 6.9x as of September 30, 2022, as shown in the chart below:

SaaS Capital Index (SaaS Capital)

Thus, by comparison, CWAN is currently priced by the market at a significant premium to the broader SaaS Capital Index, at least as of September 30, 2022.

The main risk to the company’s outlook is an increasingly likely macroeconomic slowdown or recession, which could slow sales cycles and reduce its revenue growth trajectory.

Potential catalysts for the stock’s upside could include a “short and shallow” downturn or pause in rising US interest rates leading to a rising stock market and rising AUM-based earnings. .

I’m not optimistic about the US stock market in the face of rising interest rates and rising cost of capital.

Although CWAN is essentially at operating breakeven and EPS, its stock isn’t cheap relative to a broader SaaS index, and the company’s growth rate will likely face pressure over the period. coming.

So I’m waiting for CWAN in the short term.

Comments are closed.